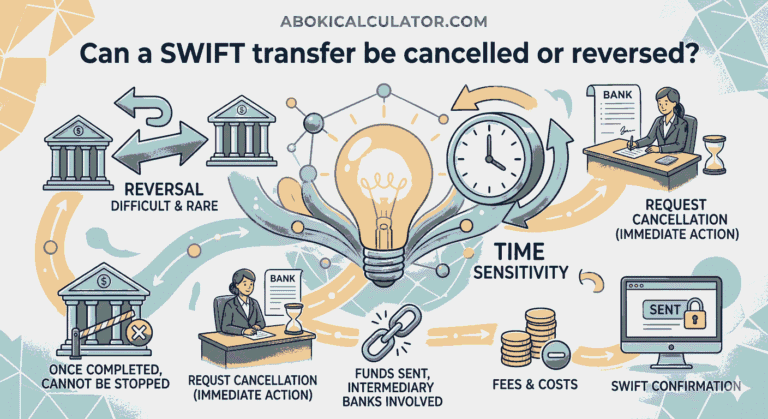

Your money is not gone. That is the most important thing to understand before anything else.

SWIFT returns, also called "return of funds" messages, are a normal part of how international transfers are corrected when something goes wrong. The money travels through banking channels, hits a problem, and gets sent back. It rarely disappears. What actually happens depends on where in the chain the failure occurred and how quickly your bank processes the return.

A SWIFT payment is returned when a bank in the payment chain, usually the receiving bank or an intermediary, cannot process the transfer and sends it back to the originating bank. This can happen within hours or take several business days, depending on how many banks are involved and how they handle exceptions.

The failure is almost always technical or administrative. Wrong account number. Missing routing detail. A compliance flag. Rarely anything you did maliciously wrong.

Why This Happens

Most SWIFT returns trace back to one of these:

- Wrong account number or IBAN. Even a single digit off will cause a return. Banks do not guess or correct. If the number does not match, they send it back.

- Incorrect or invalid BIC/SWIFT code. If the BIC code you provided points to the wrong bank, a suspended branch, or an invalid entry, the payment fails at routing.

- Account name mismatch. Some countries, particularly the UK and parts of Europe, now run strict name-matching checks. If the account name does not match the recipient's registered name, the bank rejects the transfer.

- Account closed or dormant. The recipient's account may have been closed, merged into another account, or flagged as inactive since the last time you sent money there.

- Beneficiary bank does not accept the currency. Not every bank accepts every currency. A Nigerian naira transfer to a European account that only holds euros, for example, will be returned.

- Missing or incorrect intermediary bank details. Some transfers require a correspondent or intermediary bank. If those details are absent or wrong, the payment stalls and eventually bounces.

- AML/compliance hold. The receiving bank's compliance team may have flagged the transaction based on amount, origin country, or transaction description. This can result in a return or a freeze pending documentation.

- Transfer limit exceeded. Some accounts have incoming transfer caps. If the amount exceeds what the account is configured to receive, the bank returns it.

- Sanctions or restricted country routing. If any bank in the payment chain is on a restricted list, the transaction gets blocked and returned.

What Happens to Your Money

This is what people actually want to know.

When a SWIFT payment is returned, the funds travel back through the same chain they came through. Your sending bank receives a return message (an MT103 reversal or an equivalent SWIFT message) and credits the money back to your account.

Here is the honest reality:

The money is held temporarily, not lost. While it is in transit back to you, it sits in the correspondent banking chain. This is normal.

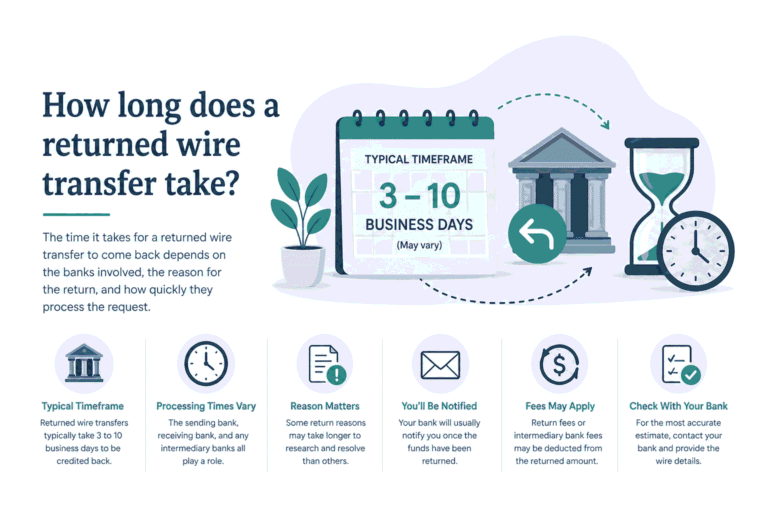

Return times vary. A straightforward return from a European bank can arrive back in two to five business days. A return from a complex multi-hop chain involving African, Asian, or Middle Eastern banks can take seven to fourteen business days.

Fees may be deducted. Your bank may charge a recall fee. The intermediary bank may deduct a processing fee. The amount you get back is sometimes slightly less than what you sent. Check your bank's schedule of charges.

The exchange rate is not guaranteed. If you converted to a foreign currency before sending, you may get back the equivalent in your local currency at the rate applied on the return date. Not the rate on the original send date.

You are not penalized. A SWIFT return does not affect your credit record or your banking relationship. It is an operational correction, not a default.

What to Do Now

Work through these steps in order.

- Call your sending bank first. Tell them the transfer was returned and ask for the SWIFT trace number (also called the UETR. Unique End-to-End Transaction Reference). This is a unique identifier that tracks your payment through the SWIFT network. Every SWIFT transfer has one.

- Request the return reason code. When a bank sends back a transfer, they include a reason code in the SWIFT message. Common codes include AC01 (incorrect account number), AC04 (closed account), and BE01 (account name mismatch). Ask your bank to tell you the exact code. This tells you precisely what to fix.

- Verify the beneficiary details independently. Do not just re-enter the same details. Get fresh confirmation directly from the recipient. Ask them to confirm their IBAN, BIC/SWIFT code, account name, and intermediary bank details (if applicable). You can cross-check SWIFT/BIC codes using the free SWIFT lookup tool on AbokiCalculator.

- Check the exchange rate impact. If you sent foreign currency and the amount returned differs, it is likely due to the exchange rate applied on the return date. Use the live exchange rate pages on AbokiCalculator to understand what rate is in play so you can reconcile the numbers.

- Wait for the funds to clear. Once your bank confirms a return is in progress, give it the expected processing window. For most returns, two to five business days. For complex routes, up to fourteen.

- Re-send only after confirming correct details. Do not resend until you have confirmed the exact failure reason and corrected the specific detail. Sending again with the same wrong information just triggers another return and another set of fees.

- Escalate if funds do not arrive within fifteen business days. If you have the trace number and the return is still outstanding after fifteen business days, contact your bank's international transfers team and request a formal investigation. They can raise this directly with the correspondent bank via SWIFT.

How to Avoid This Next Time

Validate every banking detail before you send. An IBAN that looks right can still be wrong. Before any international transfer, run the recipient's IBAN through an IBAN validator. It checks the structure, the check digits, and confirms the country format is correct. AbokiCalculator has a free IBAN validator you can use before sending.

Confirm the SWIFT/BIC code independently. Do not trust a BIC code you received by email or WhatsApp without checking it. The SWIFT lookup tool on AbokiCalculator lets you verify that a BIC is active and linked to the correct bank and branch.

Ask about intermediary banks upfront. If you are sending to certain countries, particularly in Africa, South Asia, or the Middle East, ask your bank whether a correspondent bank is required in the chain. Get those details in advance and include them in the transfer instruction.