Your money is almost certainly not gone. When a transfer leaves your account but the recipient sees nothing on their end, it almost always means the funds are sitting somewhere in the banking chain between you and them. This is one of the most common international payment problems, and in the majority of cases, it resolves without the money being lost.

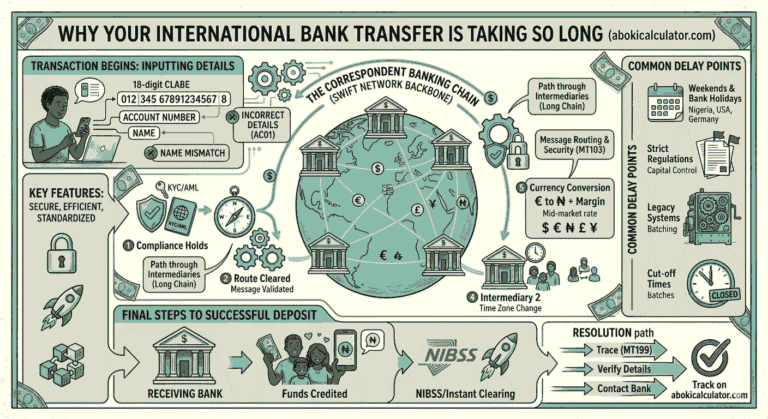

The gap between "sent" and "received" exists because international transfers do not move like a text message. Your funds leave your bank, pass through one or more intermediary banks, and then arrive at the destination bank, which then has to post the credit to the recipient's specific account. Any one of those steps can introduce a delay, a hold, or a mismatch that stops the money from appearing, even though it has technically left your account.

The key distinction to understand early: your bank showing the money as debited does not mean the recipient's bank has received it. Those are two separate events, sometimes separated by days.

Why This Happens

There are specific, identifiable reasons why a beneficiary does not receive a transfer that has already left the sender's account:

- Funds held at the destination bank pending posting. The money reached the recipient's bank but has not been credited to their account yet. Some banks, particularly in certain African, Asian, and Middle Eastern markets, take one to three additional business days to post incoming international transfers to individual accounts.

- Account number mismatch. The funds arrived at the correct bank but the account number or IBAN provided does not match any active account. The bank places the funds in a suspense account while it tries to identify the correct beneficiary or waits for instructions.

- Account name mismatch. The UK, Australia, and several European countries now run Confirmation of Payee checks, matching the account name on the transfer instruction against the name registered to the account. A mismatch results in the funds being held or returned without the recipient seeing anything.

- Intermediary bank delay. The transfer is still sitting at a correspondent bank between your bank and the destination bank. The correspondent bank may be processing high volumes, running compliance checks, or waiting for a processing window to move the funds forward.

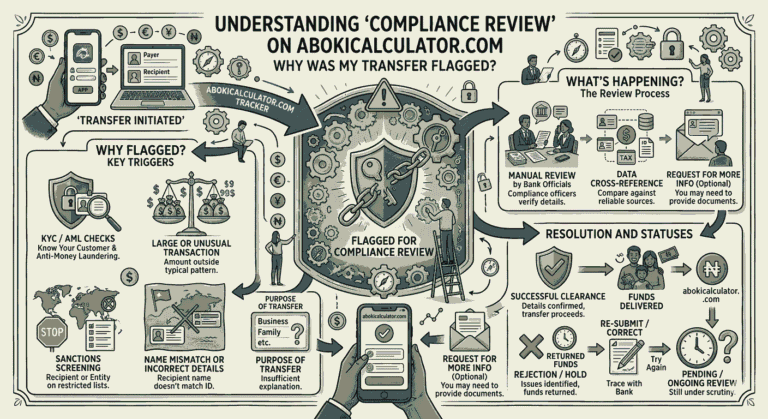

- Compliance hold at the destination bank. The receiving bank flagged the incoming transfer for internal review before posting it to the account. The recipient's balance does not update during this review period.

- Incorrect SWIFT/BIC code. The transfer was routed to the wrong bank entirely because the BIC code was incorrect. The receiving bank cannot identify the intended recipient and places the funds in a holding account.

- Currency mismatch. The sender sent a currency the recipient's account does not hold. The destination bank holds the funds pending instructions on how to handle the conversion, and the recipient sees nothing in the meantime.

- Transfer sent to a closed or dormant account. The account existed but is no longer active. The destination bank holds the incoming funds and processes a return, which takes additional time to travel back through the chain.

- Cut-off time processing. The transfer arrived at the destination bank after their daily processing cut-off and will not be posted until the next business day.

What Happens to Your Money

The money is in the banking system. It has not evaporated and it has not been stolen. The most likely scenarios, in order of frequency, are:

It is sitting at the destination bank, unposted. The bank received the funds but has not yet credited them to the specific account. This is the most common scenario and usually resolves within one to three additional business days without any action required.

It is held in a suspense account. If there was a detail mismatch, the receiving bank holds the funds in an internal suspense account while they investigate. Suspense accounts are real accounts with real money in them. The funds are safe but inaccessible until the bank resolves the discrepancy.

It is still moving through the correspondent chain. The transfer has not yet reached the destination bank. It is in transit between intermediary banks. This is normal for complex routes and typically resolves within five to seven business days.

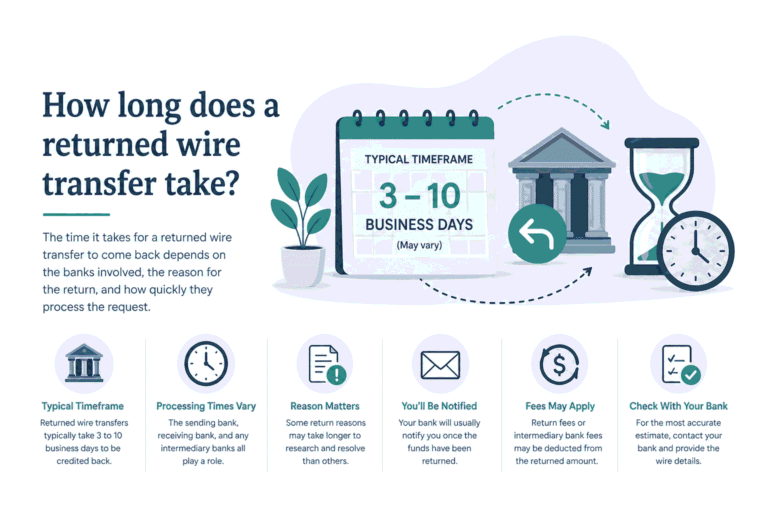

It has been returned but the return is still in transit. Some banks automatically return funds with detail mismatches without notifying either party until the return has processed. Your money may already be on its way back, but the return transfer takes as long as the original did.

Fees already charged at the time of sending are generally not reversed if the transfer fails or is returned. The amount that comes back to you may be slightly less than what you originally sent.

What to Do Now

- Confirm the exact number of business days that have passed. Do not count weekends or public holidays in either country. If it has been fewer than five business days on a standard international route, the transfer is still within normal processing time. Wait before escalating.

- Ask the recipient to check properly. Before raising an investigation, ask the recipient to confirm: the exact name on the account, whether the account accepts international transfers, whether the currency matches, and whether they have checked with their bank directly rather than just looking at their online banking balance. Some banks update branch records before online systems.

- Contact your sending bank and request the SWIFT UETR. The UETR (Unique End-to-End Transaction Reference) is the transfer's tracking number in the SWIFT network. Every international SWIFT transfer has one. With this number, any bank in the chain can locate exactly where the funds currently sit. Do not proceed without getting this reference.

- Request a SWIFT gpi trace. Ask your bank to initiate a gpi (Global Payments Innovation) trace using the UETR. This trace shows the full journey of the payment: which banks it has passed through, which bank currently holds it, and whether it has been delivered or is pending. Most major banks can run this within twenty-four hours.

- Cross-check the recipient details against what was submitted. Ask your bank for a copy of the exact transfer instruction they sent, including the IBAN or account number, the BIC/SWIFT code, and the account name. Compare this against what the recipient gave you. Even a single character difference explains most "not received" cases. You can verify BIC codes independently using the SWIFT lookup tool on AbokiCalculator.

- If the gpi trace shows funds delivered to the destination bank, the problem is between that bank and the recipient's account. At this point, the recipient needs to contact their own bank directly, provide the UETR, and ask why the credit has not been posted. The sending bank cannot chase the destination bank on your behalf beyond a certain point.

- If the gpi trace shows funds still in transit or held, ask your sending bank to raise a payment investigation request with the bank holding the funds. This is a formal interbank inquiry through the SWIFT network. Give it forty-eight to seventy-two hours to receive a response.

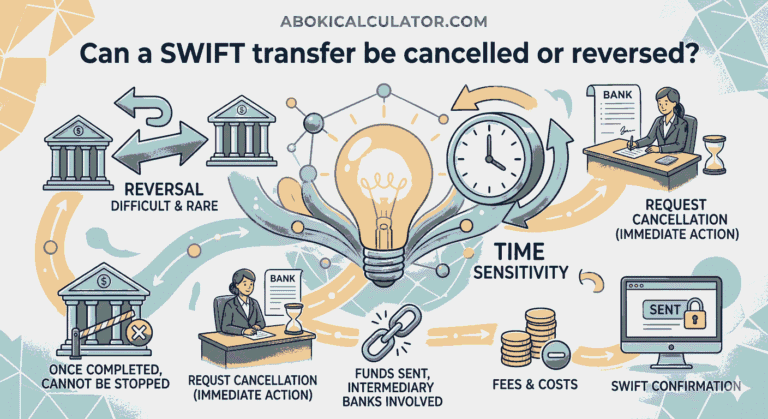

- Request a payment recall if the funds have been held for more than fifteen business days without resolution. A SWIFT gpi recall asks the holding bank to return the funds to the originating account. This takes a further five to ten business days but it starts the process of getting your money back if the transfer cannot be completed as originally instructed.

- If the transfer was returned, verify details before resending. Once the return credit appears in your account, do not just resend the same instruction. Identify what went wrong first. Validate the recipient's IBAN using the IBAN validator on AbokiCalculator and confirm the BIC is current using the SWIFT lookup tool. Sending again with the same incorrect details produces the same result.

How to Avoid This Next Time

Validate every recipient detail before initiating the transfer. Most "not received" cases trace back to a detail error that could have been caught before the money left. Before sending any international transfer, run the IBAN through the IBAN validator on AbokiCalculator. It checks the format, the check digits, and the country structure. Also verify the BIC/SWIFT code is active using the SWIFT lookup tool. A five-minute check before sending saves days of investigation afterward.

Send a small test transfer first for new recipients. If you are sending to a new account for the first time, particularly a large amount, send a small test transfer of the equivalent of five to ten dollars first. Confirm it arrives correctly before sending the full amount. This costs a small fee but protects you from the much larger cost of a failed large transfer.

Keep the transfer purpose clear and the details complete. Incomplete transfer instructions, including missing intermediary bank details or vague payment references, increase the chance of a hold or mismatch at the destination. Ask your recipient for their full banking details, including intermediary bank information if required, before you initiate. For transfers to certain countries including the US, Germany, and Australia, routing numbers, sort codes, or BSB codes may be required in addition to the account number.