Your money has not been seized and it has not disappeared. A compliance review means a bank in the payment chain has paused your transfer to verify that it meets regulatory requirements before allowing it to continue. This is a hold, not a rejection.

Banks are legally required to monitor international transfers for money laundering, fraud, sanctions violations, and other financial crimes. When a transaction triggers one of their automated screening rules, a compliance officer reviews it manually before releasing the funds. The vast majority of transfers that go into compliance review are legitimate and eventually cleared. The process just takes time.

What makes this particularly frustrating is that banks rarely explain what triggered the review. They tell you it is "under compliance review" and give you a timeline that feels vague. That is not them being difficult. Regulators actually prohibit banks from disclosing the specific details of AML screening criteria, because doing so would help bad actors design around them. So the opacity is deliberate, and it applies to everyone equally.

Why This Happens

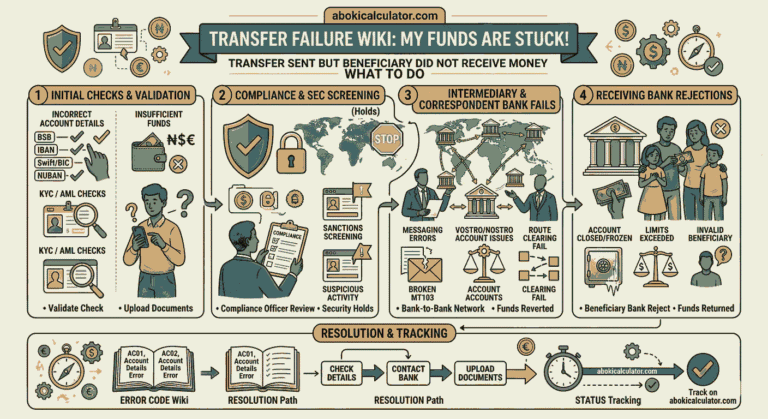

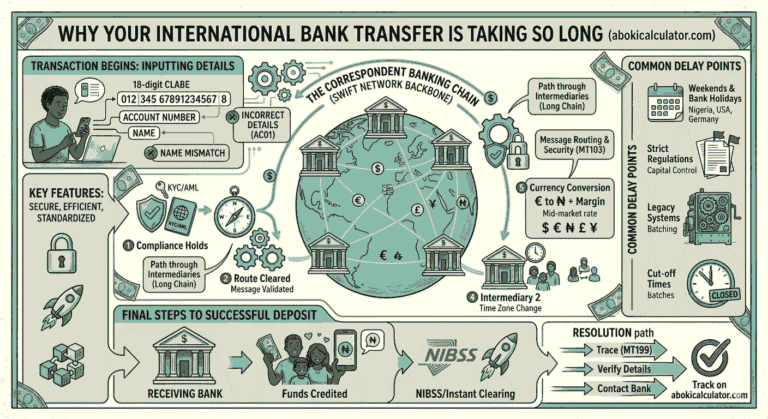

Compliance reviews are triggered by automated screening systems. These systems flag transactions based on rules, not intent. Here are the specific things that commonly trigger a review:

- Transaction amount thresholds. Large transfers, particularly those above $10,000 in the US or equivalent thresholds in other jurisdictions, automatically trigger enhanced due diligence. The threshold varies by country but the principle is the same everywhere.

- Origin or destination country risk. Nigeria, along with several other countries, is classified as high-risk by FATF (the Financial Action Task Force), the global standard-setter for AML rules. Transfers involving high-risk countries receive additional scrutiny at almost every international bank.

- Unusual transaction patterns. If your transfer amount, frequency, or destination is significantly different from your previous transaction history, the bank's system flags it as an anomaly.

- Partial name matches against sanctions lists. Banks screen sender and recipient names against sanctions lists maintained by OFAC (the US Treasury), the UN Security Council, the EU, and others. A partial match, even an accidental one caused by a common name, can trigger a manual review.

- Vague or missing transaction purpose. Many banks require a stated purpose for international transfers. If the field is left blank or filled with something generic like "personal," it can trigger a review, especially on larger amounts.

- New banking relationship. If this is one of your first international transfers, or if you are sending to a new recipient, the bank has less history to assess the transaction against. Less history means more scrutiny.

- Correspondent bank flags. Sometimes the review is not initiated by your bank but by an intermediary correspondent bank further down the chain. Their screening systems are independent and may flag transactions that your sending bank already cleared.

- Business account mismatch. If you are sending from a business account but the transaction looks personal in nature, or vice versa, compliance systems can flag it as inconsistent.

- Structured transactions. Multiple smaller transfers sent in quick succession that together add up to a large amount can trigger a structuring flag, even when the intent is entirely legitimate.

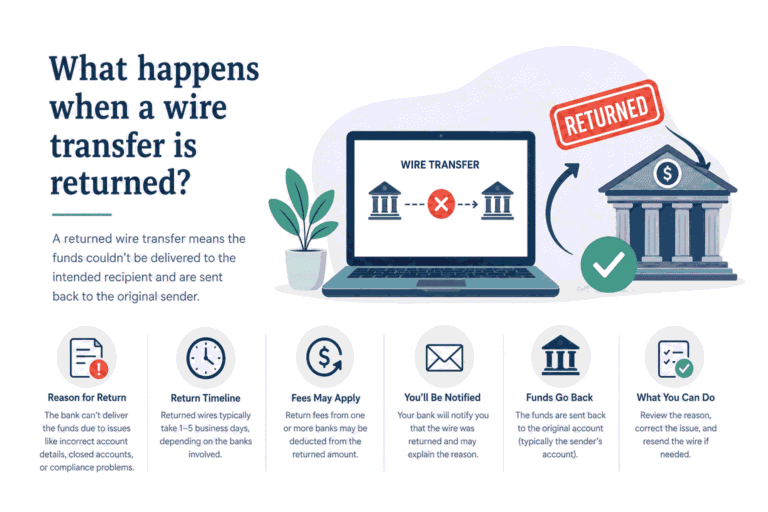

What Happens to Your Money

The funds are held in a suspense or compliance account at the bank that initiated the review. That bank, whether it is your sending bank or a correspondent bank in the chain, has physical custody of the money while the review is active.

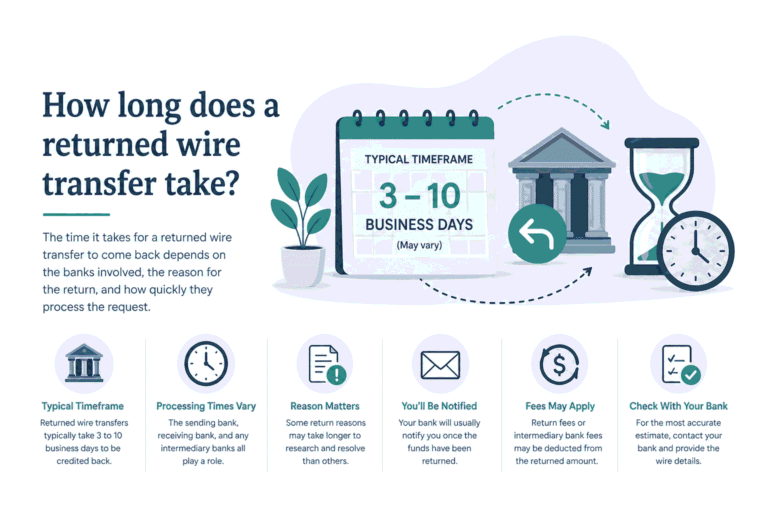

The hold is temporary in most cases. The bank reviews the transaction, determines it is legitimate, and releases it. This typically takes two to five business days for routine reviews. More complex cases, particularly those involving large amounts or high-risk corridors, can take two to three weeks.

If the bank determines it cannot process the transfer, which happens in a minority of cases, it will return the funds to the originating account. You do not lose the money. You get it back, less any fees that were already deducted.

In rare cases involving active sanctions violations, a bank may be legally required to freeze the funds and report the transaction to a government authority. This applies to actual sanctions breaches, not routine high-risk country flags. If your transfer is frozen under a sanctions order, your bank will notify you formally and you will need legal advice. This outcome is uncommon for regular personal or business remittances.

Fees already deducted at the point of sending are generally not refunded if the transfer is returned. Check your bank's specific policy on this.

What to Do Now

- Get the specific status in writing. Call your bank and ask them to confirm in writing that the transfer is under compliance review, which bank initiated the review (yours or a correspondent), and what the expected resolution timeline is. Having this in writing protects you and gives you a paper trail.

- Ask what documentation they need. Banks often release compliance holds faster when the customer proactively provides supporting documents. Ask directly: "Is there any documentation I can provide to help clear this review?" Common requests include proof of source of funds, a contract or invoice if the transfer is business-related, proof of identity, or a letter explaining the purpose of the transfer.

- Prepare your documentation now. Do not wait for the bank to formally request documents. Typical documents that speed up compliance reviews include: a bank statement showing where the funds originated, a signed letter of explanation for the transfer purpose, an employment letter or payslip if the transfer is personal income-related, or a signed invoice or contract if it is commercial.

- Do not send the money again. Some people, frustrated by the delay, attempt to cancel the original transfer and resend it. This usually creates a worse situation. The funds in review are still in the system and a second transfer can compound the problem. Wait for the first transfer to be resolved.

- Request escalation after five business days. If the review has been running for more than five business days with no update and no documentation request, ask your bank to escalate the case to their compliance team supervisor. Ask for a case reference number so follow-ups are tracked.

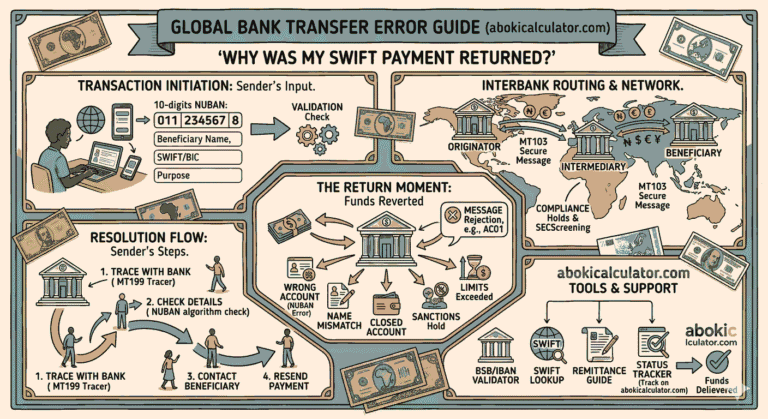

- Track the payment using your UETR. Ask your bank for the SWIFT UETR (Unique End-to-End Transaction Reference). This is your transfer's unique tracking number in the SWIFT network. With it, any bank in the chain can locate exactly where the funds are sitting. You can also use the SWIFT payment tracker on AbokiCalculator to monitor the transfer status independently.

- If the transfer is returned, confirm the correct amount before resending. When the funds come back, verify the exact amount credited, accounting for any fees deducted. If you plan to resend, make sure the recipient details are verified, especially the IBAN and BIC/SWIFT code. Use the SWIFT lookup tool on AbokiCalculator to confirm the BIC is valid before you initiate a new transfer.

- Escalate to your central bank if the hold is unreasonably prolonged. In Nigeria, if a bank is holding your international transfer without resolution for more than thirty days and you cannot get a satisfactory response, you can file a formal complaint with the Central Bank of Nigeria's Consumer Protection Department. Keep records of all communications before doing this.

How to Avoid This Next Time

Always include a clear, specific transfer purpose. When initiating an international transfer, fill in the payment reference or purpose field with something specific. "School fees payment, University of Leeds, September 2025 semester" is far less likely to trigger a review than "personal transfer." The more specific and verifiable your purpose, the easier it is for a compliance system to categorise and clear the transaction automatically.

Break unusual patterns gradually, not suddenly. If you plan to start sending larger amounts internationally, consider building up to them over a few transactions rather than sending a large amount out of nowhere. Banks use your transaction history as a baseline. A significant departure from your normal pattern is more likely to trigger a flag than a gradual change.

Verify recipient details completely before sending. Transfers that arrive at the destination bank with incorrect or incomplete details are more likely to get flagged for manual review because the bank cannot auto-match them to an account. Before every international transfer, validate the recipient's IBAN using the IBAN validator on AbokiCalculator and confirm their BIC is active using the SWIFT lookup tool. A transfer that arrives clean and complete moves through compliance screening faster.