Your money is not gone. A returned wire transfer means the funds could not be delivered and the banking system is sending them back to where they started. It is a correction mechanism, not a loss event.

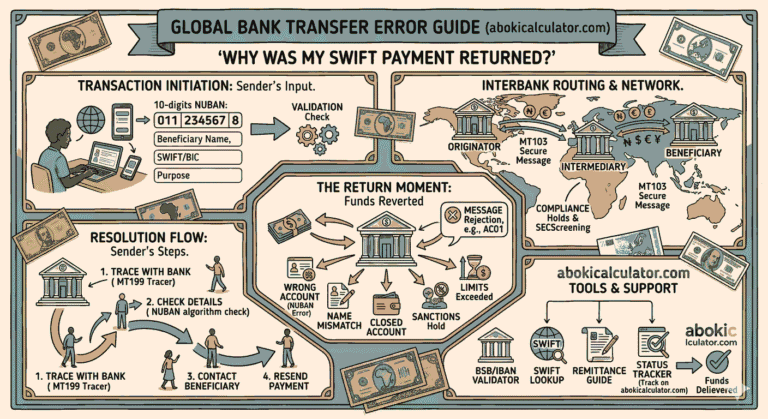

When a wire transfer is returned, a bank somewhere in the payment chain, usually the receiving bank or an intermediary correspondent bank, sends a formal rejection message back through the SWIFT network. That message instructs the originating bank to reverse the credit and return the funds to your account. The process is structured, tracked, and documented at every step.

What makes returns confusing is the timing. The money leaves your account, sometimes sits in transit for several days, and then comes back, often without a clear explanation of what went wrong. That gap between debit and return credit is where most of the anxiety lives. Understanding what is actually happening in that window makes it easier to handle.

Why This Happens

Wire transfers get returned for specific, documented reasons. Banks include a reason code in the return message, though they do not always pass that information on to you directly. These are the most common causes:

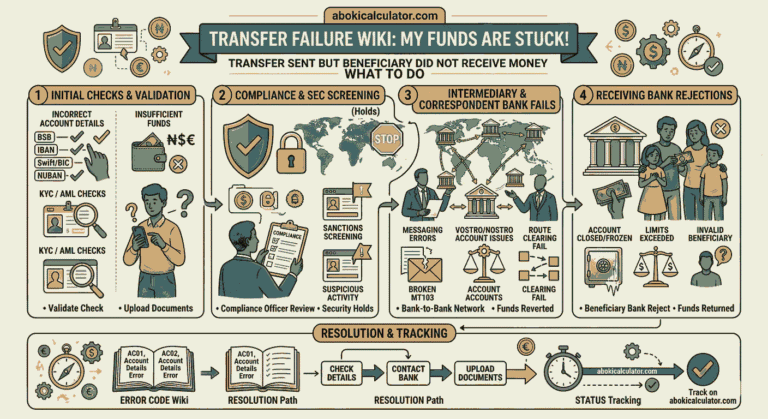

- Incorrect account number or IBAN. The most frequent cause by a distance. Even one wrong digit means the destination bank cannot match the funds to an account and sends them back.

- Account closed or dormant. The recipient's account existed when they shared the details but has since been closed, merged, or flagged as inactive. The bank cannot post to it and returns the funds.

- Account name mismatch. Several countries, including the UK and Australia, now enforce strict name-matching rules. If the name on the transfer instruction does not match the name registered to the account, the bank rejects the payment.

- Invalid or incorrect BIC/SWIFT code. The BIC code routed the payment to the wrong bank or to a branch that does not handle international transfers. The receiving institution returns it because it has no account matching the details provided.

- Currency the account cannot receive. The recipient's account only holds one currency, and the transfer arrived in another. Without instructions for conversion, the bank returns the funds rather than holding them indefinitely.

- Transfer amount exceeds account limits. Some accounts, particularly savings accounts or accounts with incoming transfer caps, cannot receive amounts above a set threshold. The bank returns anything above the limit.

- Compliance or AML rejection. The receiving bank's anti-money laundering screening flagged the transaction and the compliance team decided it could not be processed. This is less common than detail errors but does happen, particularly on high-value or high-risk corridor transfers.

- Missing intermediary bank details. Certain payment routes require specific correspondent bank information to be included in the transfer instruction. When that information is absent, the payment cannot be routed correctly and eventually bounces back.

- Beneficiary bank not reachable. In rare cases, the destination bank is temporarily offline, under sanctions, or has had its SWIFT access suspended. Payments to that bank get returned by the last reachable bank in the chain.

- Sanctioned entity match. If the recipient's name, institution, or country triggers a match against a sanctions list, the payment is blocked and returned. This applies to genuine matches, not partial name coincidences, which usually trigger a review rather than an immediate return.

What Happens to Your Money

The return process is mechanical and well-documented. Here is what actually happens:

The rejecting bank sends a return message. When a bank decides it cannot process a transfer, it generates a SWIFT return message (an MT103 reversal or equivalent ISO 20022 message) and sends it back through the same correspondent chain the original payment traveled through.

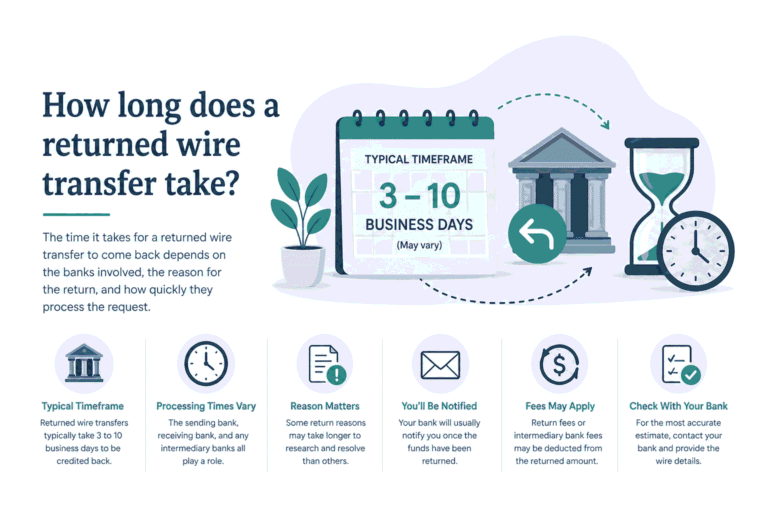

The funds travel back in reverse. The return credit passes through the same correspondent banks, in reverse order. Each bank processes the return instruction and passes it along. This is why returns take almost as long as the original transfer.

Your bank receives the return and credits your account. Once the return message completes its journey, your originating bank posts the credit back to your account. At this point, the transaction is fully reversed.

The amount you get back may be slightly less than you sent. Banks in the chain, including your own, may deduct return processing fees. Correspondent banks often charge a return fee that gets netted out of the returned amount. Some banks absorb this cost, others pass it on. Check your bank's schedule of charges.

Exchange rate differences may apply. If you converted currency at the time of sending, the return is processed at the exchange rate on the date the return credit is applied, not the original send date. If rates have moved, the naira equivalent you get back may differ from what you originally converted. Use the exchange rate pages on AbokiCalculator to check the current rate and understand what to expect.

Typical return timelines. A return from a European bank on a simple route takes two to five business days. Returns from more complex multi-hop chains, common on African, South Asian, and Middle Eastern corridors, can take seven to fourteen business days. This is normal and does not indicate a problem with the return itself.

What to Do Now

- Confirm the debit has actually posted. Before doing anything else, check your account statement and confirm the transfer was debited. If the amount is still showing as a pending transaction rather than a completed debit, the transfer may not have been sent yet and the process is simpler.

- Contact your sending bank and get the return reason code. Call the international transfers desk, not general customer service, and ask for the SWIFT return reason code included in the return message. Common codes include AC01 (incorrect account number), AC04 (closed account), BE01 (name mismatch), and RR04 (regulatory or compliance rejection). The code tells you exactly what to fix.

- Request the SWIFT UETR for the original transaction. The UETR (Unique End-to-End Transaction Reference) is the tracking number assigned to your transfer in the SWIFT network. Even for a returned transfer, this reference lets you or your bank trace the full journey and confirm the return is in progress.

- Ask for an estimated return credit date. Once your bank confirms a return is in progress, ask for the expected date the funds will appear back in your account. If they cannot give a date, ask for the maximum processing window and set a follow-up reminder.

- Do not resend until you know exactly what went wrong. Resending with the same incorrect details produces another return and another round of fees. Wait for the return to complete and identify the specific problem first.

- Verify the recipient's details independently. Contact the recipient directly and get fresh confirmation of their full banking details, including their IBAN, BIC/SWIFT code, account name exactly as registered, and any intermediary bank information required for their country. Do not re-use details from a previous message or email without confirming they are still current.

- Validate the corrected details before resending. Once you have the correct details, validate the IBAN using the IBAN validator on AbokiCalculator before you submit the new transfer. Also check the BIC/SWIFT code using the SWIFT lookup tool to confirm it is active and assigned to the correct institution. This takes five minutes and eliminates the most common causes of repeat returns.

- If the return has not arrived after fifteen business days, raise a formal investigation with your bank. Provide the UETR and ask them to trace the return through the SWIFT gpi system. Returns occasionally get stuck in the chain the same way outgoing transfers do, and a formal investigation request gets the correspondent banks to locate and release them.

How to Avoid This Next Time

Validate recipient banking details before every transfer, not just new ones. Account numbers change when people switch banks. BIC codes change when banks merge or rebrand. Details that were correct six months ago may not be correct today. Before any international transfer, run the IBAN through the IBAN validator on AbokiCalculator and confirm the BIC is still active using the SWIFT lookup tool. This takes less time than a phone call to your bank and catches the majority of return-causing errors before the money moves.

Always include the account name exactly as registered. Ask your recipient to give you their account name precisely as it appears in their bank records, not just their common name or nickname. For transfers to the UK, Australia, and increasingly other European markets, a name that does not match character for character can trigger an automatic return. Middle names, initials, and trading names all matter.

Confirm intermediary bank requirements for the destination country. Some payment corridors, particularly transfers to the United States, Canada, and parts of Southeast Asia, require additional routing information beyond the basic IBAN and BIC. Ask your bank what is required for the specific destination before sending. A transfer instruction that is missing required intermediary details will route incorrectly and either get stuck or returned.