Your money is almost certainly not lost. International transfers feel like they disappear into a black hole, but they are almost always sitting somewhere in the banking chain, waiting on a process to complete. The delay is frustrating, but it is rarely a sign that something is seriously wrong.

International bank transfers, particularly those sent via SWIFT, do not move like a domestic bank transfer. When you send money from Nigeria to the UK, Canada, or Germany, your funds pass through multiple banks before reaching the recipient. Each bank in that chain has its own processing schedule, compliance checks, and cut-off times. The result is that a transfer that should take two days can sometimes stretch to seven, ten, or even longer, without anything technically being wrong.

If your transfer has been sitting for more than three business days and you have not received any update from your bank, that is the point to start asking questions. Not before.

Why This Happens

International transfers slow down for specific, identifiable reasons. Here are the most common:

- Correspondent banking chains. Your bank likely does not have a direct relationship with the recipient's bank. Instead, your money passes through one, two, or sometimes three intermediary banks (called correspondent banks) before it arrives. Each stop adds time.

- Currency conversion processing. If the transfer involves a currency conversion, for example from naira to dollars or dollars to euros, an additional processing step is introduced. Some banks batch their conversions and only run them once or twice a day.

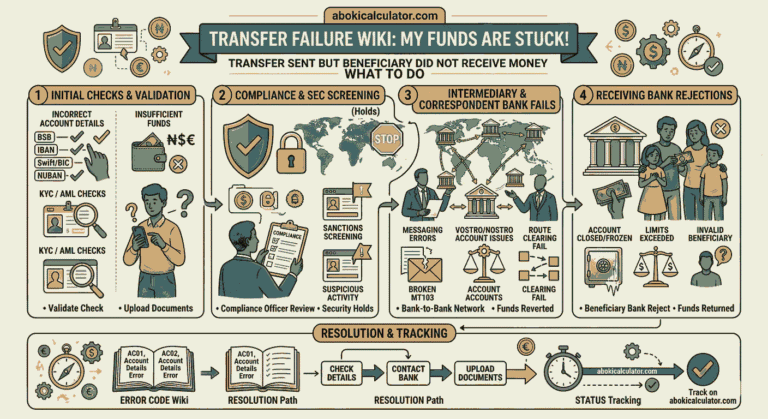

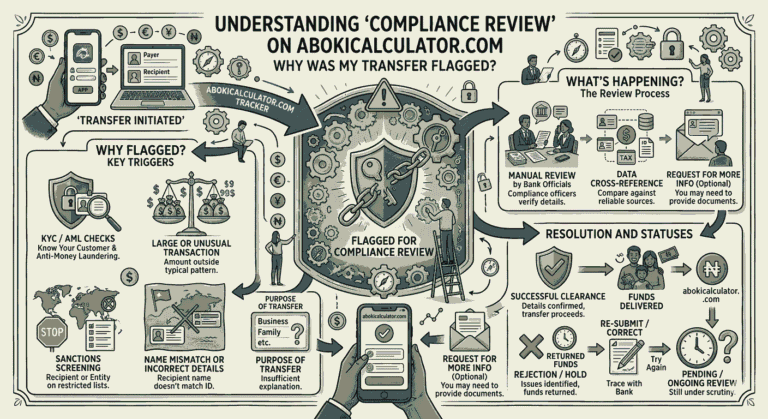

- Compliance and AML screening. Every bank in the chain runs the transaction through anti-money laundering (AML) checks. If any detail triggers a review, including the amount, origin country, or transaction description, the payment pauses while a compliance officer reviews it. This can add two to five business days.

- Sanctions screening. Transfers involving certain countries, institutions, or names go through additional screening against sanctions lists maintained by OFAC, the UN, and the EU. Even legitimate transfers can be delayed if a name partially matches a flagged entity.

- Missing or incomplete transfer details. If the original instruction lacked an intermediary bank's BIC code, a routing number, or a sort code, the receiving bank may place the funds on hold while it tries to establish where they should go.

- Bank processing cut-off times. Banks do not process international transfers 24 hours a day. Most have cut-off times, often around 3pm or 4pm local time. A transfer initiated after the cut-off on a Friday may not start moving until Monday morning.

- Public holidays. Banking holidays in either the sending or receiving country pause the chain. A transfer sent the day before a bank holiday in the destination country can sit for an extra two to three days without anyone flagging it as a problem.

- High transaction volumes. At the end of month or during peak remittance periods, banks process higher volumes of transfers. Processing times can stretch even for clean, correctly-detailed transfers.

- Beneficiary bank internal processing. Once your money reaches the destination bank, that bank still needs to credit the recipient's account. Some banks, particularly in certain markets, take an additional one to two business days to post incoming SWIFT payments.

What Happens to Your Money

While your transfer is delayed, here is where the money actually is.

It is in the banking system. Specifically, it is sitting in an account held by one of the banks in the payment chain, most likely either your bank's correspondent bank or the destination bank itself. It has not disappeared and it has not been lost.

Delays come in two types. The first is a processing delay, where the money is moving but slowly, clearing compliance checks or waiting for a business day to open. The second is a hold, where a bank has actively paused the transfer because something needs review. Your bank can usually tell the difference.

Fees may already have been deducted. Most international transfers incur charges at the sending bank, the correspondent bank, and sometimes the receiving bank. These are deducted regardless of whether the transfer is delayed. So the amount that eventually arrives may be slightly less than what you sent, even if everything is fine.

Your exchange rate is typically locked at the time of transfer. If you converted currency when you sent the money, that rate is already applied. A delay does not change the rate that was used.

What to Do Now

Work through these steps, in this order.

- Check how many business days have passed. Count only business days, not weekends or public holidays in either country. If it has been fewer than five business days, the transfer is still within a normal window for many international routes. Give it time.

- Contact your sending bank. Ask them for the SWIFT UETR (Unique End-to-End Transaction Reference). This is a 36-character tracking code assigned to every SWIFT transfer. With this code, any bank in the chain can locate the payment.

- Request a SWIFT trace (gpi trace). Since 2017, the SWIFT network has run a tracking system called SWIFT gpi (Global Payments Innovation). Your bank can use the UETR to run a gpi trace and see exactly where in the chain your money currently sits and whether it has been held. Ask them explicitly for a gpi trace, not just a general inquiry.

- Confirm the recipient's details were correct. Ask your bank to confirm the exact IBAN, BIC/SWIFT code, and account name that were submitted with the transfer. A small error in any of these details can cause the payment to stall mid-chain. You can cross-check BIC codes independently using the SWIFT lookup tool on AbokiCalculator before raising a formal inquiry.

- Ask whether a compliance hold is in place. If the trace shows the payment stopped at a specific bank, ask that bank (through your bank, as an intermediary) whether it is a compliance hold and what documentation, if any, is needed to release it.

- Escalate to the international transfers desk if needed. General customer service agents often cannot see into SWIFT traces. Ask specifically to speak with the international transfers or correspondent banking team. They have direct access to the gpi system.

- Set a follow-up deadline. If your bank confirms the transfer is in the chain but cannot give you a resolution date, ask for a forty-eight-hour update. Banks respond faster when a specific follow-up is expected.

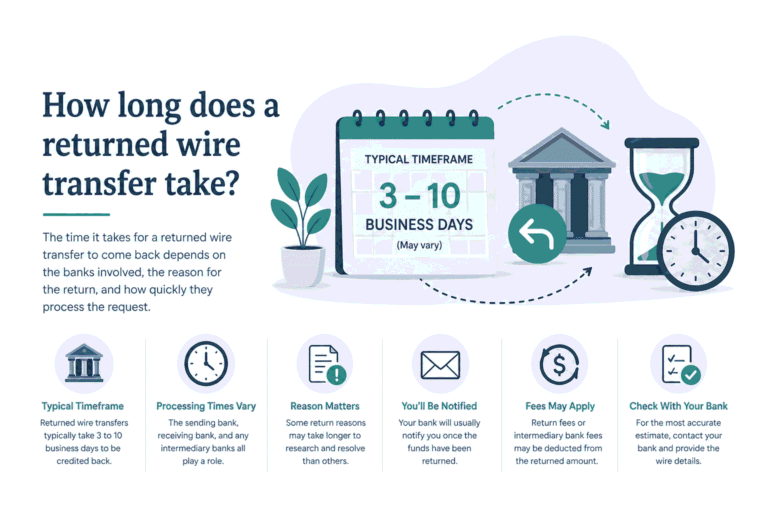

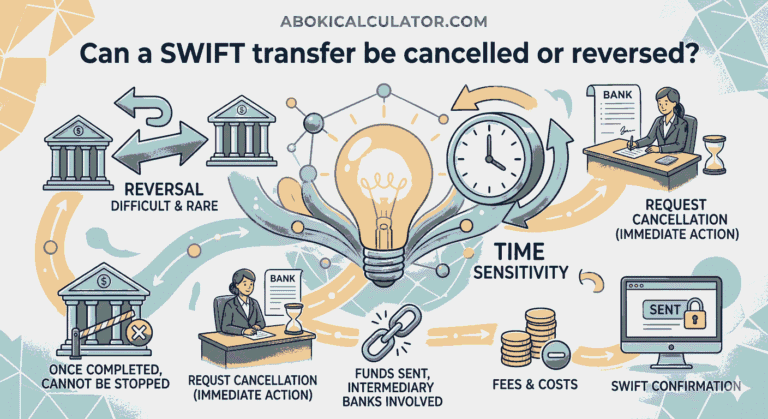

- If the transfer has been outstanding for more than fifteen business days with no resolution, ask your bank to formally recall the payment. A SWIFT recall (gpi recall request) instructs the holding bank to return the funds. This typically takes an additional five to ten business days but it starts the return process.

How to Avoid This Next Time

Verify all recipient details before you send. The single biggest cause of delayed or stalled international transfers is incorrect or incomplete beneficiary information. Before initiating any transfer, validate the recipient's IBAN using the IBAN validator on AbokiCalculator. It checks the format, the check digits, and the country structure in seconds.

Confirm the SWIFT/BIC code is active. BIC codes become inactive when banks merge, rebrand, or close branches. A BIC that worked a year ago may not work today. The SWIFT lookup tool on AbokiCalculator lets you verify that a code is current and linked to the correct institution before you submit a transfer instruction.

Send early in the week, early in the day. Transfers initiated on a Monday or Tuesday morning (in the sending bank's time zone) clear faster because they avoid weekend gaps and benefit from a full week of banking days. Transfers sent on a Friday afternoon often do not start moving until Monday. If timing matters, send before noon, midweek.

Ask your bank about correspondent banks upfront. Before sending to an unfamiliar country or a smaller regional bank, ask your bank which correspondent bank they route through for that destination. Some corridors have known delays, particularly parts of West Africa, South Asia, and the Caribbean. Knowing this in advance sets the right expectations.