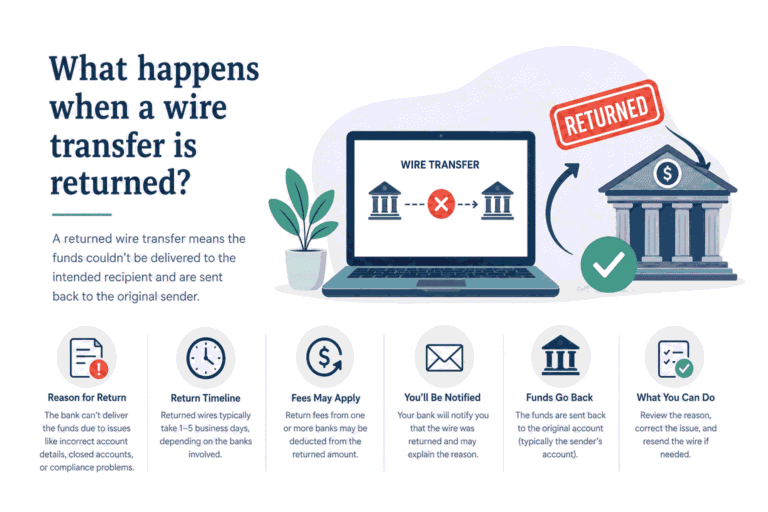

Most returned wire transfers arrive back in your account within two to ten business days. The exact timeline depends on which bank initiated the return, how many banks the payment passed through, and whether there are any holds in the return chain. Your money is not gone. It is traveling back through the same banking channels it used to get where it was going.

A wire transfer return is not instant because international payments do not move in real time. When a receiving bank or intermediary bank rejects a transfer, it generates a formal return message through the SWIFT network. That message travels back through each bank in the original payment chain, and each bank processes it in sequence before passing it along. The more banks involved, the longer the return takes.

The anxiety around this is understandable. Your account shows the money gone, the recipient has nothing, and nobody has given you a clear date. That gap is where this article focuses.

Why Returns Take Longer Than Expected

Understanding what slows down a return helps you set realistic expectations and know when to escalate.

- Multi-hop correspondent chains. If your transfer passed through two or three intermediary banks on the way out, the return has to pass back through all of them in reverse. Each bank processes the return instruction on its own schedule.

- Intermediary bank processing windows. Correspondent banks do not process international transactions around the clock. Most run one or two processing cycles per day. If a return message arrives after the cut-off, it waits until the next cycle. This alone can add one to two business days per hop.

- Weekend and public holiday gaps. Banks do not process interbank transfers on weekends or local public holidays. A return initiated on a Thursday afternoon in a European bank may not move again until the following Monday, especially if there is a holiday in either country.

- Compliance review on the return itself. Occasionally, a return is flagged for compliance screening just like an outbound transfer. This is rare but adds two to five business days when it happens.

- Currency reconversion processing. If the original transfer involved a currency conversion, the return requires a reverse conversion. Some banks batch currency operations and only process them once or twice daily, adding time to the return credit.

- Receiving bank posting delays. Even after your bank receives the return credit from the correspondent network, it still has to post the funds to your specific account. Most banks do this the same day or next business day, but some take longer depending on their internal processes.

- Return message errors. In rare cases, the return message itself contains an error, for example a missing reference number or incorrect account detail, and it gets stuck in the chain the same way the original transfer did. This requires a manual intervention and adds significant time.

- High-volume processing periods. At end of month, end of quarter, and during peak remittance seasons, correspondent banks process significantly higher volumes. Standard processing times can stretch even for clean, uncomplicated returns.

What Happens to Your Money During the Return

The money is in the banking system the entire time. It is not sitting in a grey area or an unmonitored account. Here is the precise sequence:

The rejecting bank holds the funds in a return queue. When a bank decides to return a transfer, it places the funds in an outgoing return queue and generates a SWIFT return message. The funds leave that bank's books and travel back through the correspondent chain.

Each correspondent bank processes and forwards the return. Every bank in the chain receives the return credit, verifies the instruction, and passes it to the next bank. This is the step that takes the most time, particularly on routes with multiple hops.

Your bank receives the return credit. Once the return completes its journey back to your originating bank, they post the credit to your account. At this point the transaction is fully reversed and your balance updates.

The amount returned may be slightly less than what you sent. Return processing fees are commonly deducted by correspondent banks and sometimes by your own bank. These are standard charges, not errors. Check your bank's schedule of charges to understand what deductions to expect.

The exchange rate applied to the return may differ from the original. If you converted from naira to another currency before sending, the return credit is typically calculated at the exchange rate on the date the return is processed, not the original send date. Rates move daily. Use the live exchange rate pages on AbokiCalculator to check the current rate and estimate what you will get back before the return arrives.

Realistic Return Timelines by Route

These are honest estimates based on how international correspondent banking actually operates:

- Within the same currency zone (e.g., Europe to Europe, USD to USD): Two to four business days

- Transatlantic routes (US, UK, Canada): Three to six business days

- Nigeria to Europe or North America: Five to ten business days

- Nigeria to Asia, Middle East, or smaller markets: Seven to fourteen business days

- Complex multi-hop routes with compliance holds: Up to twenty-one business days

These are return timelines, not original transfer timelines. The return starts from the moment the rejecting bank generates the return message, not from when you first sent the transfer.

What to Do Now

- Get the return confirmation from your bank. Contact the international transfers desk, not general customer service, and ask them to confirm that a return has been initiated. Ask for the return reference number or the SWIFT UETR (Unique End-to-End Transaction Reference) for the original transaction. This reference tracks both the outbound payment and the return.

- Ask for the return reason code. The bank that rejected your transfer included a reason code in the return message. Ask your bank to share it. Common codes include AC01 for incorrect account number, AC04 for closed account, and BE01 for name mismatch. Knowing the reason tells you exactly what to fix before you resend.

- Ask for an estimated return credit date. Your bank may not give you a precise date but they should be able to give you the expected processing window. Get this in writing, even via email or chat, so you have a reference point for follow-up.

- Track the return using your UETR. With the UETR in hand, you or your bank can track the return through the SWIFT gpi system. The SWIFT payment tracker on AbokiCalculator can help you monitor the status of the transfer independently while you wait.

- Do not resend the transfer while the return is in progress. Until the return credit appears in your account, the original transfer is still live in the banking system. Sending a second transfer before the first is fully resolved creates a duplicate instruction that can be difficult to unwind.

- Set a follow-up date. Based on the route your transfer used, set a calendar reminder for the outer edge of the expected return window. If you are waiting on a Nigeria-to-Europe return, set a reminder for ten business days from the date the return was initiated. If the funds have not arrived by then, escalate.

- Escalate if the return exceeds fifteen business days. Contact your bank's international transfers team and ask them to raise a formal investigation using the UETR. They can query the correspondent bank holding the return directly through the SWIFT network. Give them forty-eight hours to come back with an update.

- Reconcile the returned amount and fees. When the return credit finally posts, check it against what you sent and note any deductions. If the amount deducted in fees seems unusually high or does not match your bank's published charges, raise it with your bank and ask for a fee breakdown.

How to Avoid a Repeat Return

Verify all recipient details before sending, every time. The vast majority of wire transfer returns trace back to a detail error: a wrong digit in an IBAN, an outdated BIC code, or an account name that does not match. Before initiating any international transfer, validate the IBAN using the IBAN validator on AbokiCalculator. It checks the structure and check digits instantly and flags errors before the money moves.

Confirm the BIC/SWIFT code is still active. Banks merge, rebrand, and close branches. A BIC that worked last year may point to a suspended or reassigned entry today. The SWIFT lookup tool on AbokiCalculator lets you check whether a BIC is current and linked to the correct institution before you send.

Ask about intermediary requirements for the specific destination. Some corridors require additional routing details beyond the standard IBAN and BIC. Transfers to the United States often require an ABA routing number. Some Asian markets require additional local bank codes. Ask your bank what is needed for the specific country before sending. A transfer that arrives at a correspondent bank without the required routing information either stalls or gets returned, and either outcome costs you time and fees.