The short answer is: sometimes, but only if you act fast and the money has not yet been credited to the recipient's account.

SWIFT transfers are not like card payments or mobile transfers that can be reversed with a button tap. Once a SWIFT payment leaves your bank and enters the correspondent banking network, it is in motion. Cancelling it becomes a negotiation between banks, not a simple undo command. Whether you get the money back, and how quickly, depends on exactly where in the chain the payment currently sits.

This is not a reason to panic. Banks cancel and recall SWIFT transfers regularly. The process exists, it works, and most requests succeed when the funds have not yet been credited to the recipient. What matters is how quickly you act and whether you use the right process.

Why People Need to Cancel or Reverse a SWIFT Transfer

This section replaces "Why this happens" because the situation here is not an error in the traditional sense. It is an intentional action. These are the real-world reasons people need to cancel or reverse a SWIFT transfer:

- Sent to the wrong account. A digit was wrong in the IBAN or account number and the payment went somewhere it was not meant to go.

- Sent to the wrong person entirely. The wrong saved beneficiary was selected, or details were copied from an old transaction by mistake.

- Duplicate transfer. The same payment was submitted twice due to a system error, bank app glitch, or user error.

- Fraud or scam. The sender was deceived into transferring money to a fraudulent account and realised it after the payment was submitted.

- Wrong amount sent. The amount was entered incorrectly and the payment went through before the error was noticed.

- Change of instructions. A legitimate payment that the sender needs to stop because the underlying deal or agreement changed after the transfer was initiated.

- Bank error. The bank processed a transfer that should not have been sent, either due to a system issue or an instruction error on their side.

What Happens to Your Money

This is the part that matters most. Here is the honest picture.

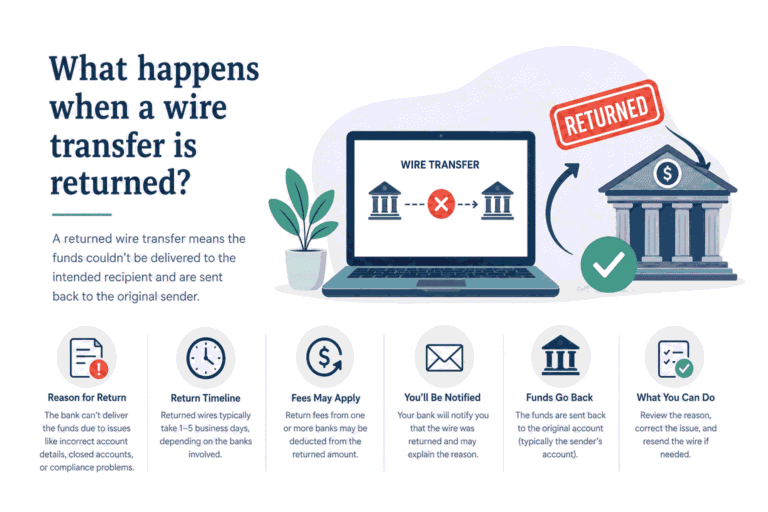

If the payment has not yet been credited to the recipient's account, a cancellation or recall is possible. The money is still in the banking chain, held by your bank, a correspondent bank, or sitting in the destination bank's incoming queue. In this state, a formal recall request can stop it before it posts.

If the payment has already been credited to the recipient, the situation changes significantly. At that point, the money is legally in the recipient's account and the bank cannot unilaterally take it back. A recall request becomes a request for voluntary return, and whether you get the money back depends entirely on whether the recipient agrees to return it.

If the recipient is a scammer, the bank will cooperate with fraud investigations and law enforcement, but recovery is not guaranteed. Speed is critical in fraud cases. The faster you report, the better the chance funds are still traceable.

Fees are charged regardless of outcome. Banks charge a recall or cancellation fee even if the attempt is unsuccessful. Correspondent banks in the chain may also deduct handling fees. You will not receive a full refund of your original amount in most cases.

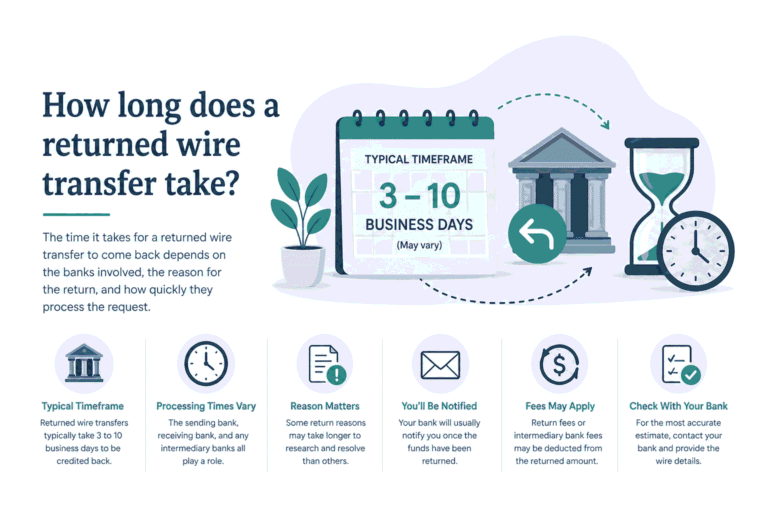

Return timelines for successful recalls. If the recall succeeds and the funds are returned, expect five to fifteen business days for the credit to appear in your account, depending on the route and how many banks are involved in unwinding the payment.

What to Do Now

Move quickly. Every hour between the transfer being sent and your bank submitting a recall request reduces the chance of success.

- Call your bank immediately. Do not use the app or send an email. Call the international transfers desk directly and tell them you need to cancel or recall a SWIFT transfer. Use the words "gpi recall request." This is the formal process in the SWIFT system and using the right terminology gets you to the right team faster.

- Have your transfer details ready. You will need the exact amount, the date and time the transfer was submitted, the recipient's bank name and account details, and ideally the transaction reference number your bank assigned when you initiated the payment.

- Ask for the SWIFT UETR. This is the Unique End-to-End Transaction Reference, a 36-character tracking code assigned to every SWIFT payment. The UETR is what your bank uses to locate the payment in the network and attach the recall request to it. Without it, the process is slower.

- Ask your bank to check gpi status before submitting the recall. If your bank has access to SWIFT gpi tracking, they can check the payment status in real time before submitting the recall. If the payment has already been credited, they will know immediately and can advise you on next steps for a voluntary return request instead.

- Submit the recall in writing as well. After the phone call, follow up with a written request by email or through your bank's secure messaging system. Include the transfer details, the reason for the recall, and the time you called. This creates a paper trail that speeds up processing and protects you if there is a dispute.

- For fraud cases, also contact your local authorities. If the transfer was made as a result of a scam, report it to the police and your country's financial regulator, not just your bank. In Nigeria, this means reporting to the EFCC and the Central Bank of Nigeria's Financial Intelligence Unit. Banks prioritise fraud-flagged recalls and can sometimes freeze the destination account while the investigation is active.

- If the recipient is known to you, contact them directly and explain the situation. A voluntary return from someone you know is faster than a formal bank recall process. Ask them to instruct their bank to return the funds. This can resolve the situation in two to three business days versus ten to fifteen for a formal recall.

- Track the recall using the UETR. Once your bank submits the gpi recall request, ask them for updates every two business days. You can also use the SWIFT payment tracker on AbokiCalculator to monitor the underlying transfer's status while the recall is in process.

- If you do not receive an outcome within fifteen business days, escalate to your bank's complaints or dispute resolution team. Ask for the recall case reference and request a status update from the correspondent bank involved. Your bank is responsible for following up with the network on your behalf.

How to Avoid Needing to Cancel Next Time

Validate every detail before confirming the transfer. The majority of accidental transfers and wrong-account situations happen because details were not checked before submission. Before sending any international transfer, run the IBAN through the IBAN validator on AbokiCalculator. It checks format, check digits, and country structure in seconds. Catching a single wrong character here costs nothing. Chasing a recall costs time, fees, and stress.

Verify the BIC/SWIFT code independently. If you received banking details from someone, especially for a large payment, do not assume they are correct. Verify the BIC code using the SWIFT lookup tool on AbokiCalculator before submitting the instruction. A BIC that points to the wrong bank sends your money in entirely the wrong direction, and recalls from incorrect routing situations are among the most complex to resolve.

Use a test transfer for new beneficiaries and large amounts. Before sending a significant payment to a new recipient, send a small test amount first. Confirm it arrives in the correct account before sending the balance. The cost of one small test transfer is negligible compared to the fees and delays involved in recalling a large misdirected payment.

Double-check beneficiary selection in your banking app. Many duplicate transfer errors happen because users select a saved beneficiary without noticing it is the wrong one, or because the app defaults to a recently used payee. Before confirming any transfer, verify the displayed account name, account number, and bank name match your current intention, not just your last transaction.