Your money has not disappeared. A Field 57 error means the transfer instruction sent by your bank was incomplete. Specifically, it was missing the details of the bank that should receive the funds on the beneficiary's behalf. Because that information was absent, the payment could not be routed correctly and was either rejected or returned before reaching the destination.

In the SWIFT messaging system, international transfers are built from numbered data fields, each carrying a specific piece of information. Field 57 is the field reserved for the "Account With Institution," which is the bank where the beneficiary holds their account. Think of it as the destination address on a parcel. If that address is missing, the courier cannot deliver it and sends it back.

This is a technical error at the instruction level, not a problem with your money itself. The funds are either still at your bank, held by a correspondent bank, or already returned. None of those outcomes mean the money is gone.

Why This Happens

Field 57 errors are almost always caused by incomplete or incorrectly structured transfer instructions. Here are the specific reasons this field ends up missing:

- Beneficiary bank details not provided. The most direct cause. When you initiated the transfer, the account with institution field, meaning the recipient's bank name and BIC/SWIFT code, was left blank or not captured by the sending bank's system.

- Bank system did not auto-populate the field. Some banking platforms attempt to derive Field 57 from other details like the IBAN. If the derivation fails, for example because the IBAN belongs to a smaller bank the system does not recognise, Field 57 is left empty in the outgoing SWIFT message.

- Intermediary bank routed the payment without completing the field. If the transfer passed through a correspondent bank that repackaged the SWIFT message for onward transmission, that bank may have failed to populate Field 57 correctly in the new message.

- Recipient shared incomplete banking details. The person you are sending money to may not have provided their bank's BIC or SWIFT code, only their account number or IBAN. Without the BIC, Field 57 cannot be populated.

- Branch-level BIC not included. Some banks, particularly in Europe, have a head office BIC and separate branch-level BICs. If the transfer instruction uses the head office BIC but the account sits at a specific branch that requires its own identifier, Field 57 is considered incomplete by the receiving bank's system.

- Currency-specific routing requirement not met. Certain currency corridors, particularly USD payments clearing through the US banking system, require specific routing details in Field 57 beyond a standard BIC. If those details are missing, the payment fails at the clearing stage.

- Outdated or invalid BIC used. The BIC entered in Field 57 exists but has been deactivated, reassigned, or changed due to a bank merger or rebranding. The receiving network rejects it as unresolvable.

- Online banking form did not capture the field. Some retail banking interfaces do not surface all SWIFT message fields to the customer. If the form your bank uses does not include a field for the recipient's bank BIC separately from their account number, Field 57 may never get populated in the underlying message.

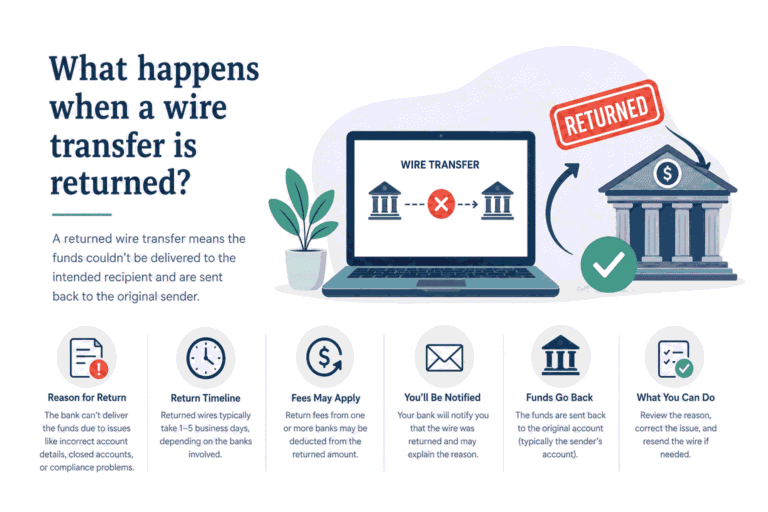

What Happens to Your Money

The transfer is either held or already returned. Here is the precise picture depending on where in the chain the error was caught.

If caught at your sending bank before transmission: The payment was rejected internally before entering the SWIFT network. Your funds are still in your account or in a pending queue at your bank. No correspondent bank fees have been deducted. This is the easiest situation to resolve.

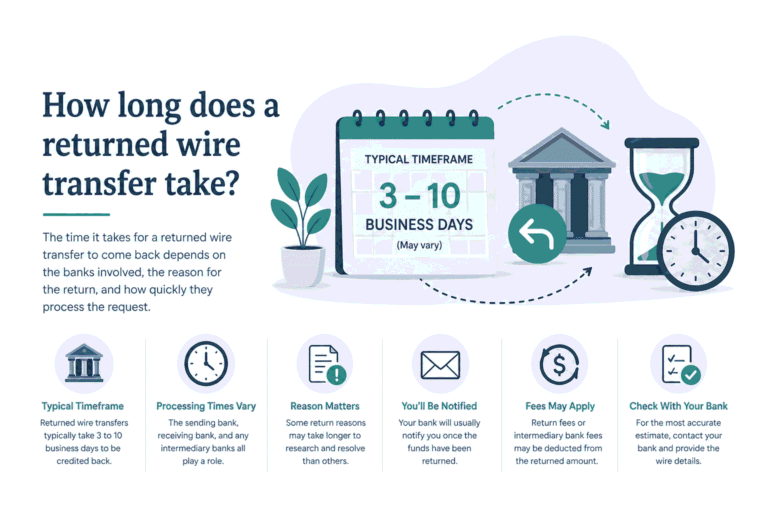

If caught by a correspondent bank mid-route: The payment entered the network, moved to a correspondent bank, and was rejected there because Field 57 could not be resolved. The funds are held at that correspondent bank pending return instructions. A return is typically initiated within one to three business days, and the funds travel back through the same chain. Expect the return credit in your account within five to ten business days.

If caught by the destination bank: The payment reached the recipient's bank but was rejected because the Field 57 details did not match any account or routing instruction the bank could process. The destination bank holds the funds briefly and then initiates a return. Same timeline. Five to ten business days for the return to complete.

In all three cases, fees may be deducted. Correspondent banks charge for handling even failed transactions. Your sending bank may also charge a return processing fee. The amount you get back can be slightly less than what you sent.

The exchange rate applied when you converted currency is locked at the time of the original transaction. If the funds are returned, your bank converts them back at the rate on the return date. Rate movements between those two dates can affect the naira equivalent you receive back.

What to Do Now

- Contact your bank's international transfers desk immediately. Ask them to confirm whether the transfer was rejected at the sending stage or is in the process of being returned from further in the chain. Also ask them to confirm whether Field 57 was populated in the outgoing SWIFT message and if not, why.

- Get the SWIFT UETR for the original transfer. The UETR (Unique End-to-End Transaction Reference) is the tracking ID assigned to every SWIFT payment. With this code, your bank can locate the payment in the network and confirm its current status. Write it down and keep it for every follow-up conversation.

- Request the exact error message or return reason code. A Field 57 error will be referenced in the SWIFT rejection or return message. The exact wording varies by bank system, but common references include "Field 57 missing," "account with institution not specified," or "BIC required for routing." The specific code tells you and your bank precisely what needs to be corrected.

- Get the correct beneficiary bank BIC from the recipient. Contact the person you are sending money to and ask them to provide their bank's BIC/SWIFT code directly from their bank's official documentation, not from memory. Ask specifically whether their account is at a branch with a separate BIC or at the head office. You can then verify that BIC is active and correctly assigned using the SWIFT lookup tool on AbokiCalculator before you resend.

- Confirm whether additional routing details are required for the destination. For USD payments routed through the US, ask your bank whether an ABA routing number is also needed alongside the BIC. For UK GBP transfers, a sort code is standard. For Australian payments, a BSB number may be required. These details populate Field 57 and related fields and their absence is a common root cause of this error.

- Wait for the return to complete before resending. Do not submit a new transfer instruction with the corrected details until the original payment has been returned to your account and the funds are confirmed back in your balance. Sending again while the first transfer is still in the return chain creates a duplicate instruction that is difficult to manage.

- Resend with a complete instruction. Once you have the correct BIC and any additional routing details, rebuild the transfer instruction from scratch. Do not copy the previous instruction and edit it. Start fresh to ensure no incomplete fields carry over. Confirm with your bank that Field 57 is populated in the outgoing message before it is transmitted.

- Follow up if the return has not arrived within fifteen business days. Provide your bank with the UETR and ask them to trace the return through the SWIFT gpi system. Returns occasionally stall mid-chain the same way outbound payments do, and a formal trace request locates them.

How to Avoid This Next Time

Always obtain the recipient's full bank details, not just their account number. An account number or IBAN alone is not sufficient for many international transfers. Before sending, confirm the recipient's BIC/SWIFT code, whether their account is at a branch with a separate BIC from the head office, any additional local routing codes required for the destination country, and the exact registered account name. This information populates Field 57 and related fields correctly and prevents the error from occurring at the source.

Verify the BIC before you submit the transfer. A BIC that looks correct can still be inactive, reassigned, or pointing to the wrong institution after a bank merger or rebranding. The SWIFT lookup tool on AbokiCalculator lets you verify that a BIC is currently active and linked to the correct bank before you commit the funds. One check before sending eliminates the most common cause of Field 57 errors.

Check country-specific routing requirements upfront. Different countries require different routing fields alongside the BIC. The US needs an ABA routing number for domestic clearing. The UK requires a sort code. Australia uses a BSB number. Canada uses a transit number. Ask your bank what is required for the specific destination country before initiating the transfer. Many banks have a country-by-country requirements guide available through their international transfers desk or website.